If you’re running a business in the UK, or planning to, understanding VAT is non-negotiable. In the UK, value-added taxation can be confusing, particularly for newcomers. Compulsorily or willingly (voluntarily) adding VAT to your sales means that the type and amount of VAT you charge will depend on your offer and the applicable VAT rates.

Quick Answer

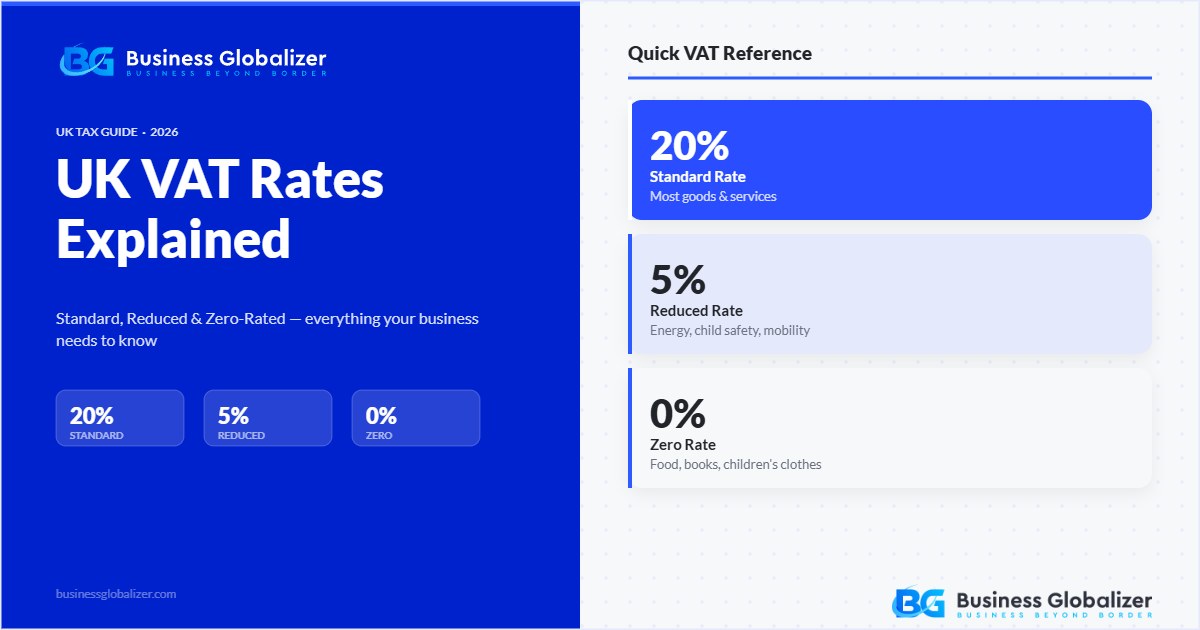

The UK has three main VAT rates: standard rate (20%) applied to most goods and services, reduced rate (5%) for items like domestic energy and children’s car seats, and zero rate (0%) for essentials like most food, books, and children’s clothing. Businesses with a taxable turnover above £90,000 must register for VAT. Understanding which rate applies to your products or services is essential for legal compliance and accurate pricing.

As a consumer, you’ve encountered VAT before, but its impact might feel fuzzy when you are a newbie to VAT registration. The goods or services you provide dictate how much VAT you charge customers, which is sent off to HM Revenue & Customs based on specific VAT rates.

So, what exactly are these UK VAT rates? Unsure how it works? Let’s learn together!

Defining the UK VAT Rates

The percentages by which value-added tax (VAT) rates are calculated and which are applied to the cost of products and services in order to ascertain the requisite payment of VAT. Asserted incrementally at each stage of the supply chain, from the procurement of raw materials to the ultimate sale to the consumer, VAT is a consumption tax.

However, the responsibility for collecting VAT and adding the applicable VAT charge to the goods or services sold in the UK lies with businesses operating within the supply chain.

Different Kinds of VAT Rates in the UK

You may be curious as to whether the VAT rate is variable or whether it is fixed. VAT rates differ in the United Kingdom according to the category of goods or services provided. In the United Kingdom, three distinct categories of VAT rates exist:

- Standard Rate.

- Reduced Rate.

- Zero Rate.

Now that you are familiar with the VAT rate classifications, we shall examine the nuances of each VAT rate:

- Standard Rate of VAT: The standard VAT rate in the UK, currently set at 20%, applies to most goods and services. It’s the default rate charged on taxable supplies unless specifically classified otherwise.

This 20% charge is usually added to the price of goods or services by businesses. It is sent to HM Revenue & Customs along with their VAT reports after they have collected it from clients. - Reduced Rate: Certain goods and services in the UK qualify for a reduced VAT rate, set at 5%. This reduced rate aims to provide benefits or support to specific industries or items. Examples of items that may fall under the reduced rate of VAT in the UK include:

- Energy-saving materials for residential properties.

- Children’s car seats.

- Certain types of renovations to residential properties.

- Zero-rated VAT in the UK: Zero-rated products and services are those that are not subject to the value-added tax (VAT) at 0%. These commodities are subject to a 0% tax rate and are not exempt from VAT. Included among the numerous services and products exempt from taxation are:

- Most food items (excluding certain items like alcoholic drinks and confectionery)

- Books and newspapers.

- Public transport fares.

Understanding these distinctions helps businesses apply appropriate VAT rates accurately, ensuring compliance while potentially benefiting from reduced or zero rates for specific products or services.

| Rate | Percentage | Applicable Goods or Services |

|---|---|---|

| Standard Rate | 20% | All goods or services not included in the reduced rates, VAT exempt or zero-rated VAT. |

| Reduced Rate | 5% | * Installation of energy-saving materials. Fuel and electricity for home heating, Goods, or services funded by grants. Contraceptive products: Contraception products, unless provided as part of medical or surgical treatment in a hospital or state-regulated institution. Car seats, carry cots, and safety seats for children. Mobility aids for the elderly. Renovations or alterations of qualifying dwellings Smoking cessation products. products for quitting smoking, including gum or patches |

| Zero Rate | 0% | Except for a few exceptions, most food items are zero-rated. Talking books and wireless sets for people with disabilities Equipment or aids for disabled people Some initial supplies of residential real estate made by a developer Sewerage services and water Caravans and houseboats that meet certain criteria may be eligible for a zero rating. Printed books, newspapers, magazines, picture and painting books for kids, sheet music, maps, and other printed materials are all zero-rated. Books, newspapers, magazines, and other comparable electronic supplies are also acceptable if they do not primarily contain advertising, music, or video. Transactions of Gold Prescription medications, drugs, equipment, and assistance for people with disabilities The first issue of banknotes by the Bank of England, Scottish banks, and Northern Irish banks Specific imports and exports, including zero-rated machine tools, supplies related to defense projects, and items delivered before the arrival of an import entry, are exempt from tariffs. Children’s clothing and footwear: Protective equipment, including a cycle helmet Women’s sanitary products |

| Additional Note | Energy-saving materials installation services are zero-rated in England, Wales, and Scotland from April 1, 2022, to March 31, 2027. After March 31, 2027, the reduced rate of 5% will apply. Businesses planning installations spanning this deadline should factor the rate change into their pricing and contracts. |

Examples of Different UK VAT Rates

Now that you are familiar with the nuances of each VAT rate let’s go through some practical examples:

- Standard Rate: For instance, Sarah is an independent software developer who registered for VAT. She typically adds the standard rate of VAT in the UK on top of her service charges.

Recently, Sarah invoiced a client £3,500 + VAT for developing a custom software solution.

Here’s the breakdown:

£4,200 = £3,500 + 20% of £3,500

After deducting the VAT payable to HMRC, Sarah keeps £3,500 for her labor.

When Sarah files her VAT return, she reports this £700 VAT to stay compliant with HMRC.

- Reduced Rate: Suppose Sarah runs a business that installs energy-saving materials in residential properties, such as insulation or solar panels. These installations qualify for the 5% reduced VAT rate.

She invoices a customer £500 + VAT for installing loft insulation. Calculating the VAT at the reduced rate: £500 + (5% of £500) = £525

Out of this total, £25 is the VAT owed to HMRC. Sarah retains the £500 for her business. By correctly applying the reduced rate to eligible energy-saving installations, Sarah ensures compliance while keeping costs lower for her customers.

- Zero Rate: Let’s follow Alex, a bookshop owner operating within the realms of zero-rated VAT in the UK. Zero-rated VAT applies to certain goods and services, including books.

Alex recently sold a variety of books to customers, totaling £1,000.

For zero-rated items, the calculation differs:

£1,000 + (0% of £1,000) = £1,000

In this case, the entire £1,000 from book sales goes straight into Alex’s earnings. Since books fall under the zero-rated VAT category, these sales have no additional VAT charges.

For Alex, this means he doesn’t owe any VAT on the books sold, aligning perfectly with the zero-rate VAT in the regulations for these specific goods.

This example showcases how Alex navigates the zero-rated VAT scenario, understanding that certain items, like books, have no VAT attached, allowing him to sell these goods without additional tax implications.

A Few More Calculation Scenarios Worth Knowing

The examples above show how to add VAT to a price, but what if you already have the total and need to work backwards? Say a customer paid £840 for a service, and you need to know how much of that was VAT.

Simple. Divide the total by 1.20 (for the standard rate), and you get the net price: £700. The remaining £140 is your VAT. For the reduced rate, divide by 1.05 instead.

One more scenario: what if a single invoice covers items at different VAT rates? Don’t average it out. Calculate the VAT for each item separately and then add them together. For example, if you’re selling a book (zero-rated) and a piece of software (standard-rated) on the same invoice, the book carries no VAT, and the software carries 20%. Each line item stands on its own.

Getting these right keeps your VAT returns clean and saves you from headaches during an HMRC audit.

Changes in UK VAT Rates

Need help with UK VAT compliance for your non-resident business? Our specialists help international entrepreneurs navigate UK tax requirements, VAT registration, and annual filings.

The journey to the UK’s VAT rates has significantly changed since their introduction in 1973. Initially set at a rate of 10%, VAT exempted essential goods like food, fuel, and housing, while other goods and services were charged at this rate.

However, subsequent alterations led to varied VAT rates. Let’s look back!

- 1974–76: The standard rate of VAT in the UK dropped to 8%, and a higher rate of 25% was introduced for select items like gasoline, which later expanded to cover non-essential goods.

- 1976–79: The higher rate decreased to 12.5%.

- 1979–92: Margaret Thatcher’s government abolished the higher rate, setting a unified standard rate of 15%, nearly doubling the previous standard rate.

- 1992–94: The standard rate increased to 17.5%.

- 1994–97: VAT on domestic fuel and power began, initially at a reduced rate of 8%, which later remained controversially low.

- 1997–2009: The Labour government reduced VAT on domestic fuel and power from 8% to 5%, where it has remained ever since. The standard VAT rate continued unchanged at 17.5% throughout this period.

- 2008–2011: In order to boost the economy following the financial crisis, the VAT was momentarily lowered from 17.5% to 15%. To address the budgetary deficit, it dropped to 17.5% before rising to 20% in 2011.

- 2020–2022: The country has more control over UK VAT rates after Brexit. The minimum VAT rate of 15% set by the EU no longer applies to the country. This means that the UK government can determine its own VAT rates, such as the standard, reduced, and zero rates.

Temporary VAT reductions were one notable change, nevertheless, especially during the COVID-19 epidemic. For instance, there was a brief decrease in VAT for a few businesses, including tourism and hospitality, beginning in July 2020. In April 2022, this reduction was once again added to the base rate.

Apart from temporary adjustments due to crises or economic stimuli, the VAT structure has remained consistent, with a few reclassifications and changes to specific goods and services, maintaining a similar structure to the standard rate of 20% established in 2011.

Functions of the UK VAT Rate

We’ve talked about the different types of VAT rates, from standard to reduced and zero rates, and explored examples of how they apply in various scenarios. But how does the UK VAT rate system function in its entirety?

From exemptions to registration thresholds and the Flat Rate Scheme, one of the different VAT schemes, there’s a lot more intricacy within the VAT system that impacts businesses. But how do these aspects relate to the VAT rates we’ve discussed? How does the UK VAT rate system function in its entirety? Let’s find out!

Exempt Goods and Services

Certain goods and services fall outside the scope of VAT, termed ‘VAT exemption.’ These include essential items like:

- Most financial and insurance services

- Most health and medical services provided by registered practitioners

- Most education and training services

- Burial and cremation services

- Rental of residential properties

These aren’t subject to VAT. While they contribute significantly to daily life, they don’t incur VAT charges.

Note: Food, domestic fuel, and housing are not exempt; they are zero-rated, which is a different classification. Zero-rated businesses can still reclaim input VAT; exempt businesses cannot. This distinction has real implications for VAT returns and should not be confused.

VAT Registration Threshold

VAT registration becomes mandatory for a business when its taxable revenue reaches a specific threshold as determined by HM Revenue & Customs. This annual threshold is £90,000. VAT collection and return to HMRC are obligations of businesses that have enrolled for VAT on taxable sales.

Flat Rate Scheme in the UK

Small businesses can use the Flat Rate Scheme to simplify their accounting for VAT. Rather than computing it for every transaction, it enables businesses to pay HMRC back with VAT, a fixed portion of their earnings.

Relationship with VAT Rates

Although exempt services and products do not incur VAT, they are not the same as zero-rated items. However, the VAT rate applicable to zero-rated services and products is 0%. Zero-rated item transactions are included in VAT returns, but at a rate that avoids additional tax being imposed.

The VAT registration threshold determines when businesses enter the VAT system but doesn’t directly influence VAT rates. Nevertheless, after registering, businesses must pay the appropriate VAT rates on their taxable sales.

On the other hand, the Flat Rate Scheme offers an alternative method for VAT accounting but doesn’t alter the standard, reduced, or zero rates themselves.

Understanding these components of the VAT system provides businesses with a clearer perspective on their VAT obligations, exemptions, and potential schemes designed to simplify their VAT accounting processes.

How Much Is the VAT Rate on UK Exports to the EU?

Since Brexit, UK VAT rules for exports to the EU have been clearly established:

- Business-to-business or B2B: Exports of goods from the UK to EU VAT-registered businesses are treated as zero-rated for UK VAT purposes. The EU business handles VAT in their own country through the reverse charge mechanism.

- Business-to-Consumer (B2C): When selling goods directly to EU consumers, UK businesses do not charge UK VAT. Instead, the importer is responsible for paying import VAT and any applicable duties in their own country. For digital services sold to EU consumers, UK businesses may need to register for VAT in each EU country where they have customers, or use the EU’s One Stop Shop (OSS) scheme.

For services (rather than goods), the general rule is that B2B services are taxable where the customer belongs, meaning UK VAT generally does not apply to services exported to EU business customers.

Finally, it is advised to refer to the official guidelines of the UK government or speak with tax experts specializing in international commerce and VAT legislation for the most up-to-date and accurate information on VAT rates for UK exports to the EU following Brexit, including any adjustments or modifications.

Key Takeaways

- Standard rate (20%) applies to most UK goods and services

- Reduced rate (5%) covers domestic energy, children’s car seats, and some home improvement materials

- Zero rate (0%) applies to most food, books, children’s clothing, and public transport

- VAT registration threshold is £90,000 taxable turnover; businesses exceeding this in any 12-month rolling period must register for VAT with HMRC.

- Exports outside the UK are generally zero-rated; EU rules changed post-Brexit

FAQs

Q1: What is the VAT rate in the UK for digital services and goods providers?

Answer: The VAT standard rate of 20% applies to providers of digital products and services based in the United Kingdom. However, regardless of whether the customer is situated within or outside the United Kingdom, the VAT rate that applies to these services or commodities may vary under specific circumstances.

Q2: What is the VAT rate in the UK for health and education services?

Answer: Health and education services in the UK are generally exempt from value-added tax (VAT).

Q3: How much does UK VAT cost businesses that are part of the flat rate scheme?

Answer: Companies enrolled in the UK Flat Rate Scheme to HMRC pay a fixed VAT rate generally lower than the standard 20% VAT rate. This rate is industry-specific.

Q4: What is the VAT rate on bank charges in the UK?

Answer: In the UK, bank charges are not subject to VAT. This implies that companies are exempt from charging VAT on bank transactions. This is so because bank fees are regarded as financial services and, in the UK, financial services are not subject to VAT.

Final Thoughts

VAT doesn’t have to be the headache it’s made out to be. Once you know which rate applies to what, and why, the rest falls into place fairly naturally. Whether you’re charging the standard 20%, applying a reduced rate on eligible goods, or selling zero-rated items, getting it right from the start saves you from costly corrections later.

When in doubt, HMRC’s guidance is always your safest reference point. And if you’re running a UK business as a non-resident, having the right support makes all the difference.

Operating a business in the UK as a non-resident? Business Globalizer helps with UK company setup, VAT registration, and ongoing compliance — all handled remotely.